Imagine being able to forecast stock market movements with a level of precision that feels almost unfair. Not by guessing, not by reacting late to breaking news, but by uncovering patterns buried so deeply in market data that today’s most powerful classical computers struggle to see them in time. This is the promise behind quantum computing stock market predictions — and it’s no longer a distant science fiction idea.

For decades, investors, traders, and analysts have chased better models for predicting price movements. We’ve seen technical indicators, fundamental analysis, machine learning, and deep neural networks all attempt to tame the chaos of financial markets. Each innovation delivered progress, yet markets remain noisy, uncertain, and brutally complex. Classical computers, no matter how fast, still process information one step at a time. When datasets explode in size and variables interact in non-linear ways, even advanced systems hit practical limits.

Quantum computing changes the rules of that game. Instead of relying on traditional bits that are either a zero or a one, quantum systems use qubits — units of information that can exist in multiple states at once and influence one another in ways classical logic cannot replicate. This allows quantum machines to explore vast numbers of possible outcomes simultaneously, making them uniquely suited for problems filled with uncertainty, probability, and optimization. In other words, problems that look a lot like the stock market.

In recent years, quantum finance has quietly moved from theory into experimentation. Financial institutions, research labs, and technology companies are no longer asking whether quantum computing can help markets — they are testing how. Early pilot programs now focus on risk modeling, portfolio optimization, derivatives pricing, and pattern recognition across massive historical datasets. These efforts are still in their early stages, but the results are compelling enough to attract serious investment and long-term commitment.

At the heart of these breakthroughs are qubits. Through phenomena such as superposition — where a qubit can represent multiple values at once — and entanglement — where qubits become mathematically linked across distance — quantum systems unlock exponential computational possibilities. For stock market prediction, this means evaluating countless market scenarios, correlations, and risk paths in parallel rather than sequentially.

This article explores how that power is being applied in practice. Rather than vague hype or speculative promises, we’ll examine seven concrete ways qubits are transforming stock market prediction models. From faster Monte Carlo simulations to quantum-enhanced machine learning and real-time arbitrage detection, each section connects the technology to real financial use cases, realistic timelines, and measurable advantages for traders and long-term investors alike.

Quantum computing may not replace classical finance models overnight, but it is steadily reshaping how predictions are made. For those paying attention, the shift has already begun.

Quantum Computing in Finance: From Theory to Market Experiments

The idea of using quantum computing in finance did not begin with stock trading dashboards or hedge fund experiments. It started quietly in academic research, where physicists and mathematicians explored how quantum algorithms could outperform classical ones in probabilistic simulations. One of the earliest areas of interest was Monte Carlo simulation, a technique heavily used in finance to model uncertainty, risk, and future price distributions. Researchers quickly realized that many financial problems shared the same mathematical structure as problems quantum computers were designed to solve efficiently.

As quantum hardware matured, financial institutions took notice. Markets are complex systems driven by countless interacting variables — interest rates, macroeconomic signals, company fundamentals, sentiment, and global events. Classical systems process these inputs sequentially, which makes exploring every possible interaction extremely time-consuming. Quantum computing, by contrast, evaluates many potential states of a system simultaneously, offering a new approach to modeling uncertainty at scale. This is precisely why quantum computing stock market predictions became an early focus of applied quantum research.

In recent years, the financial sector has shifted from theoretical curiosity to practical experimentation. Rather than waiting for fully fault-tolerant quantum machines, institutions began working with hybrid quantum–classical models. In these setups, classical computers handle data ingestion and preprocessing, while quantum processors tackle the hardest mathematical components — optimization, sampling, and probability estimation. This hybrid approach allows real-world testing today while preparing for more advanced systems in the future.

Finance is a prime candidate for quantum advantage because it is dominated by three types of problems: uncertainty, optimization, and pattern recognition. Stock market prediction depends on evaluating millions of possible futures, balancing risk against return, and detecting weak signals hidden in noisy data. These challenges scale exponentially as markets grow more interconnected. Quantum systems thrive in exactly this environment, where exploring many outcomes at once is more valuable than computing a single answer quickly.

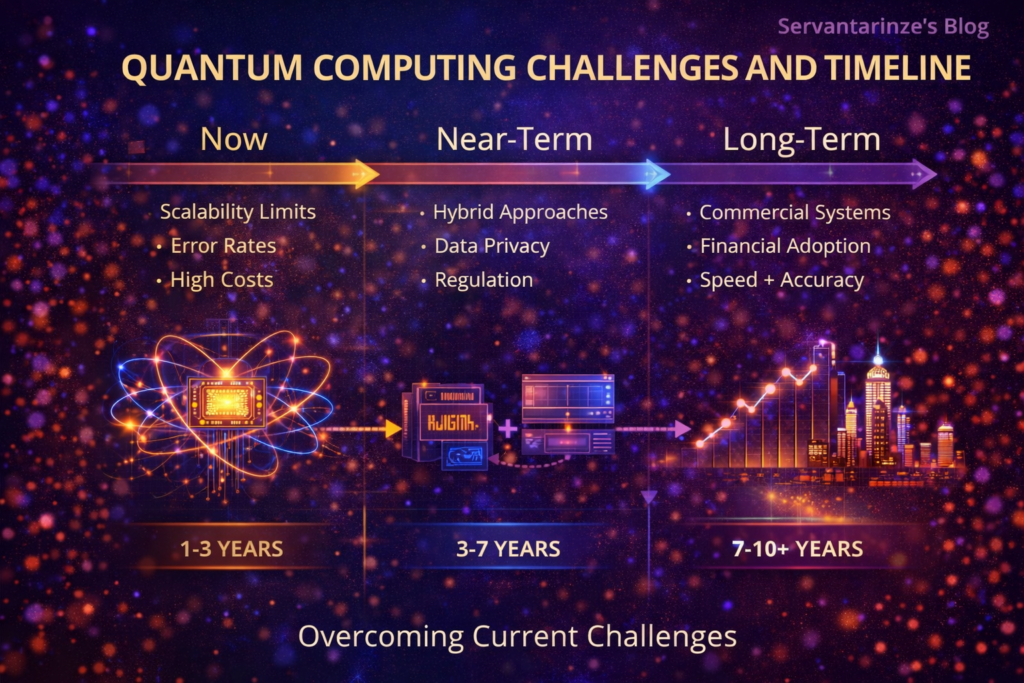

That said, it is important to remain realistic. Current quantum machines are still limited by noise, short coherence times, and a relatively small number of usable qubits. Error rates remain a challenge, and most systems require specialized environments such as cryogenic cooling. However, steady progress in error mitigation, qubit stability, and algorithm design continues to push practical boundaries forward. Instead of waiting for perfection, financial researchers are learning how to extract value incrementally.

The most credible outlook is a gradual transition rather than a sudden disruption. Over the coming years, hybrid quantum-classical systems will continue to deliver targeted advantages in specific financial tasks. As hardware improves and algorithms mature, these advantages will expand into broader areas of forecasting and market analysis. Understanding this trajectory is essential for separating genuine innovation from exaggerated claims.

With this foundation in place, we can now explore the most impactful applications in detail. The following sections break down seven specific ways qubits are already reshaping how stock market predictions are modeled, tested, and refined.

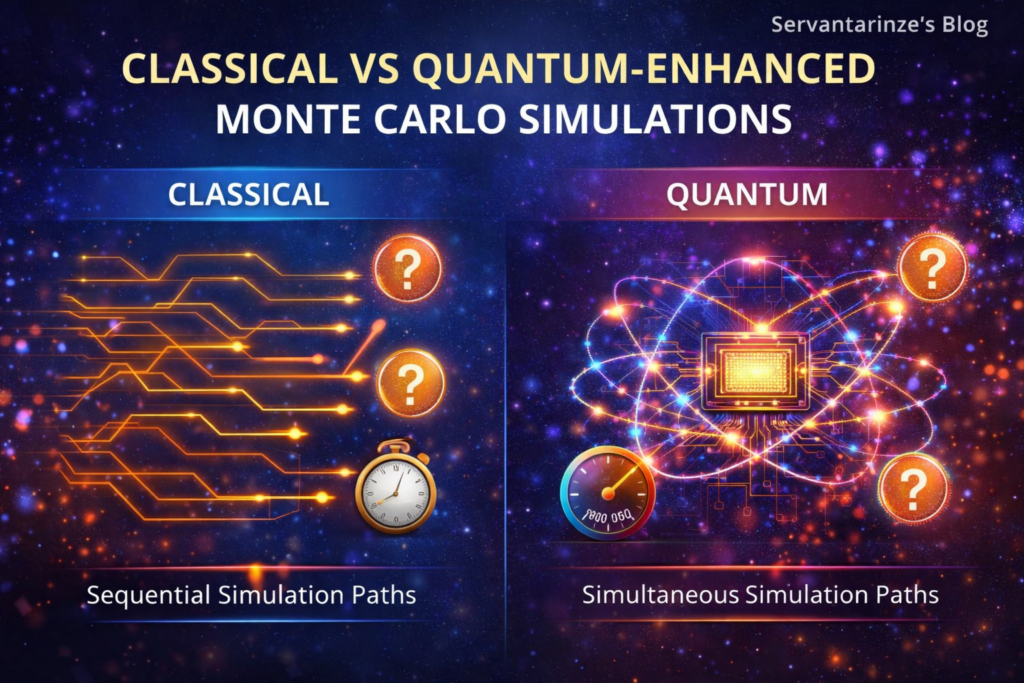

1. Enhanced Monte Carlo Simulations for Risk Forecasting

Monte Carlo simulations sit at the core of modern financial forecasting. They help analysts estimate future price movements by running thousands or millions of possible market scenarios, each based on different assumptions about volatility, interest rates, and correlations. The limitation is speed. Classical computers must process these scenarios one after another, which makes large-scale simulations slow and costly, especially during periods of market stress.

Quantum computing approaches this problem differently. By using qubits in superposition, quantum systems can evaluate many potential outcomes at the same time rather than sequentially. This dramatically accelerates probability-based calculations and allows risk models to explore deeper layers of uncertainty. In the context of quantum computing stock market predictions, this means more accurate estimates of downside risk, tail events, and extreme market behavior.

Financial institutions experimenting with quantum-enhanced Monte Carlo methods have already reported promising results. Derivative pricing, value-at-risk calculations, and stress testing models can be executed faster while maintaining precision. For traders and portfolio managers, this translates into better risk awareness during volatile markets, where delayed information often leads to costly decisions.

The long-term implication is profound. Faster simulations allow firms to test strategies more frequently, adapt to market changes in near real time, and avoid overexposure to hidden risks. Instead of reacting after losses occur, quantum-enhanced models move forecasting closer to prevention.

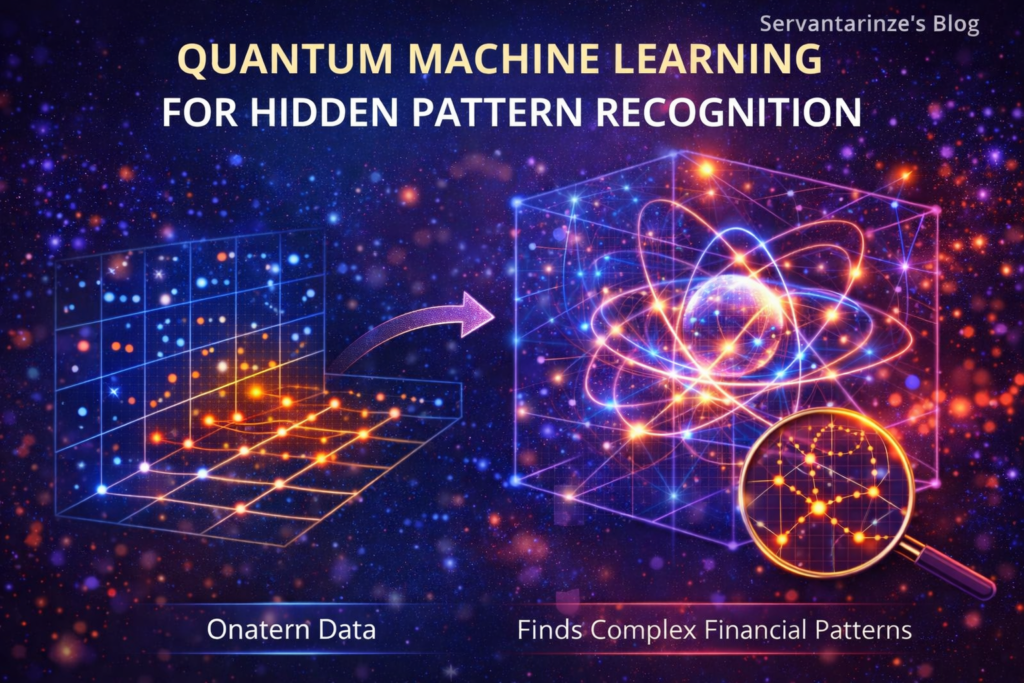

2. Quantum Machine Learning for Hidden Pattern Recognition

Machine learning has already reshaped market analysis by identifying patterns across historical price data, volume metrics, and technical indicators. However, classical machine learning struggles when relationships become highly non-linear or when datasets grow beyond manageable dimensions. Financial markets are full of such complexity, where small signals are often buried beneath noise.

Quantum machine learning introduces new mathematical tools that expand pattern recognition beyond classical limits. Algorithms such as Quantum Support Vector Machines can map financial data into higher-dimensional spaces, revealing correlations that traditional models overlook. This capability is particularly valuable for stock market prediction, where subtle relationships often precede major price movements.

What makes this approach especially powerful is its potential to identify rare or emerging patterns rather than just repeating historical ones. In practical terms, this opens the door to earlier detection of regime shifts, structural market changes, or unusual trading behavior. These insights are critical for both long-term investors seeking stability and active traders searching for timing advantages.

As hybrid quantum-classical workflows mature, quantum machine learning is likely to complement existing models rather than replace them outright. Classical systems still excel at data preparation and feature extraction, while quantum components enhance the deepest layers of analysis. Together, they create a more flexible and adaptive prediction framework.

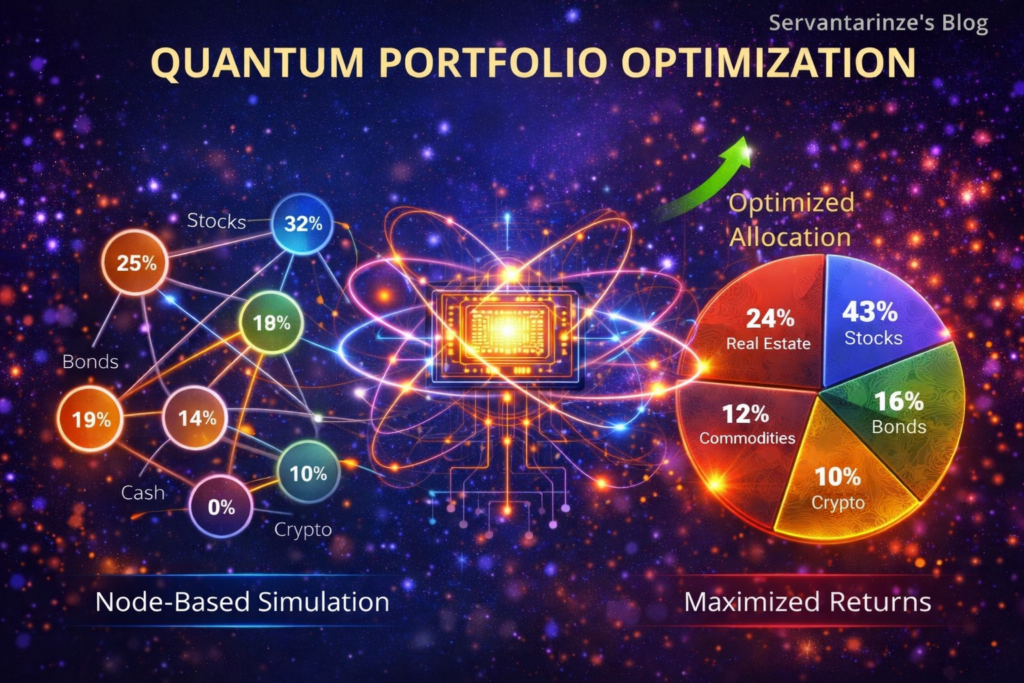

3. Optimized Portfolio Allocation and Rebalancing

Portfolio optimization is one of the most mathematically demanding problems in finance. Investors must balance expected return against risk while accounting for constraints such as asset correlations, liquidity, and transaction costs. As the number of assets increases, the number of possible portfolio combinations grows exponentially, quickly overwhelming classical optimization methods.

Quantum algorithms approach this challenge by treating portfolio construction as a global optimization problem rather than a series of approximations. Using techniques designed to explore many solutions simultaneously, quantum systems can identify asset allocations that better balance risk and reward. For quantum computing stock market predictions, this means forecasts are not evaluated in isolation but as part of a dynamically optimized investment strategy.

Early experiments in quantum-enhanced portfolio optimization suggest improved diversification and more resilient performance during periods of market uncertainty. Rebalancing decisions can also be executed more efficiently, reducing unnecessary trading while maintaining strategic alignment. Over time, this leads to lower costs and more consistent outcomes.

For institutional investors and asset managers, the appeal lies in scalability. As portfolios become more complex and global, quantum optimization offers a path to managing that complexity without sacrificing precision. It represents a shift from reactive allocation to proactive, data-driven portfolio design.

4. Faster Option Pricing and Derivatives Valuation

Options and complex derivatives are among the most computationally intensive instruments in financial markets. Their pricing depends on multiple interacting variables, including volatility, time decay, interest rates, and underlying asset behavior. Classical pricing models often rely on approximations or simplified assumptions to remain computationally feasible, especially during periods of high market volatility.

Quantum computing offers a different path by accelerating probability estimation at the heart of derivatives pricing. By evaluating multiple price paths simultaneously, quantum-enhanced models can compute expected payoffs more efficiently than classical simulations. In the context of quantum computing stock market predictions, this allows traders to assess risk and opportunity with greater precision when markets are moving fast.

The practical benefit is responsiveness. Faster and more accurate pricing enables real-time adjustments to hedging strategies, reducing exposure during sudden price swings. For institutional desks managing large derivatives books, even small improvements in pricing accuracy can translate into significant cost savings over time.

As quantum hardware continues to mature, derivatives valuation is expected to remain one of the earliest areas where measurable financial advantages emerge. It sits at the intersection of uncertainty modeling and speed, making it a natural fit for quantum acceleration.

5. Improved Time-Series Forecasting with Quantum Neural Networks

Financial markets generate vast streams of time-series data, from price movements and trading volumes to macroeconomic indicators. Forecasting trends within this data is challenging because financial signals are noisy, non-stationary, and often influenced by external shocks. Classical neural networks have improved forecasting accuracy, but they still struggle with long-range dependencies and unstable patterns.

Quantum neural networks introduce new ways of encoding and processing temporal information. By leveraging quantum states to represent complex probability distributions, these models can capture subtle dynamics that classical networks overlook. This enhances trend detection and improves the reliability of forward-looking signals used in stock market prediction.

For investors, the advantage lies in adaptability. Quantum-enhanced time-series models are better suited to environments where historical patterns evolve rather than repeat. This makes them valuable tools for identifying emerging trends early, before they become obvious to the broader market.

While these models are still largely experimental, ongoing research continues to demonstrate steady improvements. Over time, quantum neural networks are expected to complement classical forecasting systems, especially in scenarios where noise and uncertainty dominate.

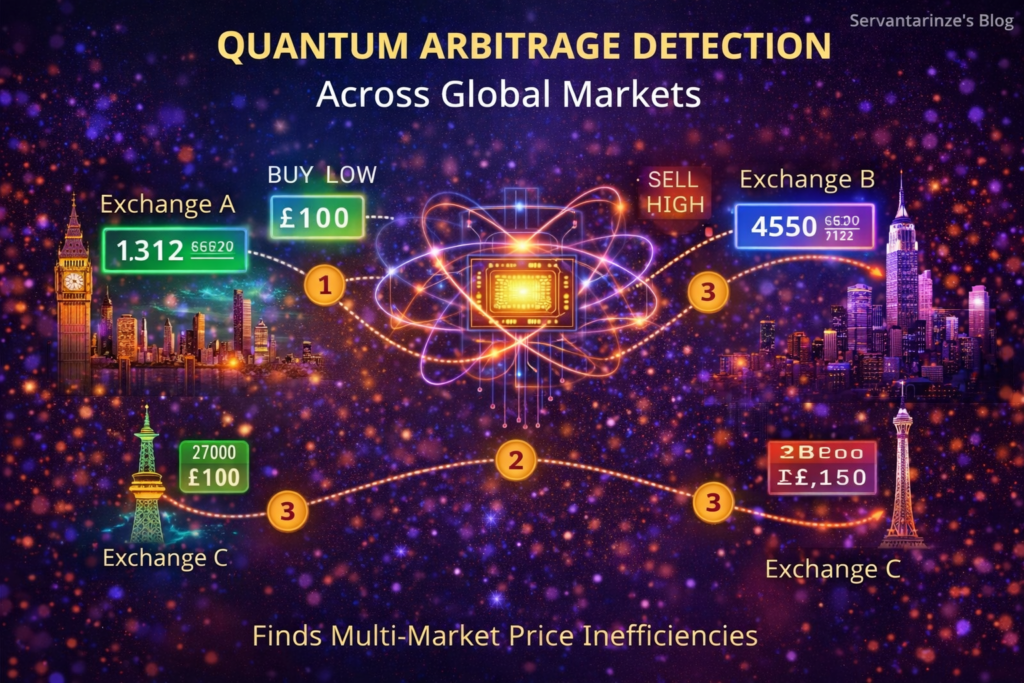

6. Arbitrage Detection Across Global Markets

Arbitrage opportunities exist when price discrepancies appear across markets, exchanges, or asset classes. These opportunities are often fleeting, disappearing within fractions of a second as traders exploit them. Detecting arbitrage at scale requires analyzing massive amounts of real-time data under extreme time constraints.

Quantum computing introduces a powerful advantage by allowing simultaneous analysis of multiple market states. Through entanglement, qubits can represent correlated assets across different exchanges, enabling faster identification of pricing inefficiencies. For quantum computing stock market predictions, this capability enhances short-term forecasting accuracy and execution timing.

High-frequency trading firms stand to benefit the most from this application. Sub-second detection of arbitrage opportunities can provide a decisive edge in competitive markets. Even outside high-frequency contexts, improved arbitrage analysis contributes to more efficient pricing and reduced market friction.

As global markets become increasingly interconnected, the value of cross-market analysis continues to grow. Quantum-enhanced arbitrage detection offers a scalable approach to navigating this complexity.

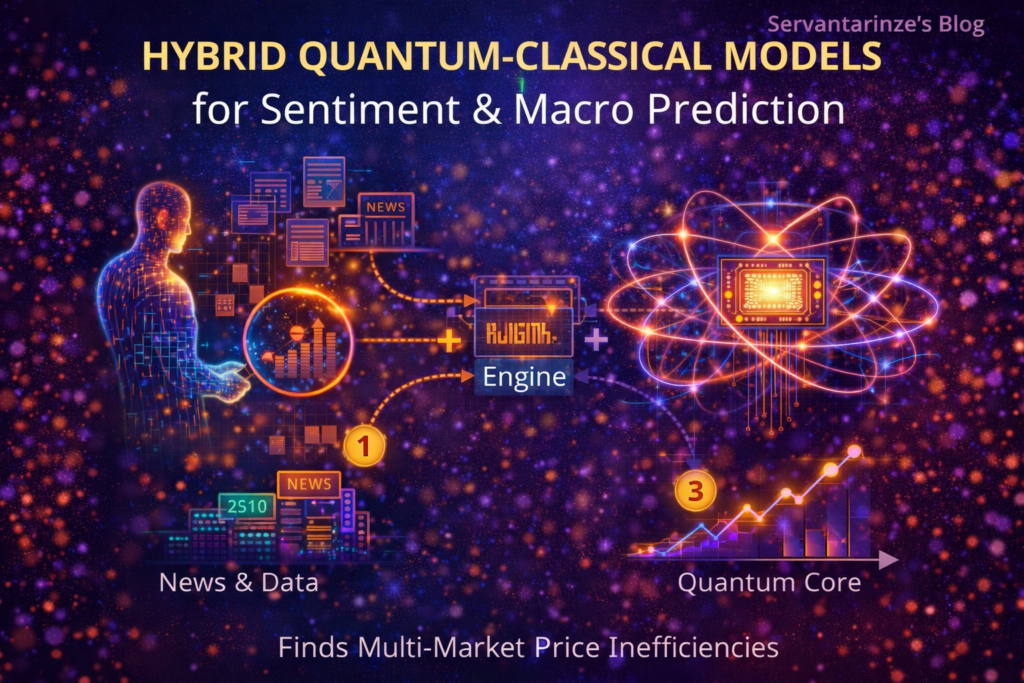

7. Hybrid Quantum-Classical Models for Sentiment and Macro Forecasting

Stock prices are influenced not only by numerical data but also by human behavior. News headlines, economic reports, and investor sentiment all shape market movements in ways that are difficult to quantify. Classical sentiment analysis tools extract signals from text and social data, but integrating these signals into predictive models remains challenging.

Hybrid quantum-classical systems offer a more holistic approach. Classical algorithms handle text processing and sentiment extraction, while quantum components analyze how these signals interact with market variables at scale. This integration improves macro-level forecasting and strengthens the foundation of quantum computing stock market predictions.

The long-term vision is a unified forecasting framework that blends technical indicators, fundamental data, and sentiment signals into a single predictive model. Early research suggests that such hybrid systems could significantly reduce forecasting error by capturing interactions that classical models treat independently.

As computational capabilities advance, these hybrid models are expected to play a central role in next-generation market analysis. They reflect a shift away from isolated indicators toward truly integrated prediction systems.

Challenges and a Realistic Timeline for Quantum Finance

Despite its promise, quantum computing is not a magic solution that instantly solves the stock market. Current quantum systems still face meaningful limitations. Qubits are fragile, highly sensitive to environmental noise, and difficult to scale reliably. Most quantum processors require extreme operating conditions, such as cryogenic temperatures, which makes deployment expensive and technically demanding.

Another challenge lies in integration. Financial markets rely on vast, continuously updating datasets, and quantum machines do not yet handle raw data ingestion efficiently. This is why hybrid quantum-classical systems dominate current experimentation. Classical computers manage data pipelines and real-time feeds, while quantum processors focus on the most computationally demanding tasks. This division of labor is effective, but it also limits how broadly quantum advantages can be applied today.

There is also an important ethical and structural consideration. Advanced quantum tools are expensive, and early access is largely limited to major institutions with deep resources. If left unchecked, this could widen existing gaps between large financial players and smaller participants. As quantum finance matures, questions around fairness, transparency, and regulation will become increasingly important.

The most realistic outlook is gradual progress rather than sudden disruption. In the near term, quantum-enhanced models will continue to deliver advantages in specific areas such as risk modeling, optimization, and probabilistic forecasting. Over the coming decade, as hardware improves and error correction advances, these advantages are expected to expand into broader applications. Understanding this timeline helps separate genuine innovation from exaggerated expectations.

Conclusion: Why Quantum Computing Will Redefine Market Prediction

Quantum computing is quietly reshaping how financial markets are analyzed and understood. Rather than replacing classical systems outright, it introduces a new layer of intelligence — one that excels at uncertainty, complexity, and scale. Through qubits, financial models can explore more possibilities, uncover deeper patterns, and adapt more quickly to changing conditions.

The seven approaches explored in this article illustrate how quantum computing stock market predictions are evolving from theoretical concepts into practical tools. From faster risk simulations and improved portfolio optimization to advanced pattern recognition and sentiment-aware forecasting, each application targets a core weakness of classical finance models. Together, they form a foundation for more resilient and forward-looking market analysis.

For traders, analysts, and long-term investors, the key takeaway is not to expect instant perfection, but to recognize direction. The institutions and individuals who understand quantum finance early will be better positioned to evaluate its impact, adopt it responsibly, and integrate it intelligently as the technology matures.

Qubits are not just transforming computation. They are changing how probabilities are explored, how risk is measured, and how future market behavior is anticipated. As quantum systems continue to evolve, the way we predict and profit from financial markets will evolve with them.

What to Do Next

If you want to stay ahead of this transformation, now is the time to build foundational knowledge. Explore how quantum computing works, follow developments in quantum algorithms, and understand where hybrid systems are already delivering value. The future of finance will not belong solely to those with the fastest hardware, but to those who understand how to use it wisely.

Subscribe for more deep-dive tutorials on quantum computing, emerging technologies, and their real-world applications. Share your thoughts in the comments: do you believe quantum systems will redefine market prediction, or will classical models remain dominant longer than expected?

Quantum finance is still unfolding — and those who learn early will shape what comes next.

Related Quantum Computing Guides You May Find Useful

If you want to deepen your understanding of how quantum technologies are reshaping computing, security, and global innovation, the following guides expand on key areas closely connected to quantum finance and market prediction.

Quantum Encryption: 7 Powerful Ways It Keeps Your Data Safe

As quantum computing advances, traditional encryption methods face increasing pressure. This guide explains how quantum encryption works, why it matters for data security, and how next-generation cryptographic techniques are being developed to protect sensitive information in a post-quantum world.

Quantum Cloud Computing: 9 Powerful Ways the Cloud Is Accelerating the Quantum Era

Access to quantum hardware is rapidly expanding through cloud platforms. This article explores how quantum cloud computing is lowering barriers to experimentation, enabling hybrid quantum-classical workflows, and accelerating real-world adoption across finance, research, and enterprise applications.

Quantum Startups: 14 Game-Changing Companies You Should Know

Behind many breakthroughs in quantum technology are fast-moving startups pushing innovation forward. This resource highlights leading quantum startups, what they are building, and how their technologies could influence industries ranging from finance and healthcare to cybersecurity and materials science.

Together, these resources provide a broader view of the quantum ecosystem — from secure communication and cloud access to the companies driving the next wave of innovation.

Authoritative External Reference

For readers who want a deeper, research-backed perspective on how quantum computing is expected to impact financial modeling, risk analysis, and forecasting, the following external resource provides valuable industry-level insights.

How Quantum Computing Could Transform Financial Services

This analysis from the World Economic Forum explores how quantum computing may influence financial markets, risk modeling, portfolio optimization, and broader financial services infrastructure, offering a balanced view of opportunities, limitations, and realistic adoption pathways.